In business practice, especially at retail stores, supermarkets, or individual business establishments, customers frequently purchase goods without requesting invoices. However, according to new regulations effective from June 1, 2025, sellers are still required to issue electronic invoices for retail customers who do not request invoices. Failure to comply with this requirement may result in penalties for businesses and affect subsequent tax declarations.

So specifically, how to issue invoices for retail customers who do not request invoices in compliance with the law and tax data standards? Let’s explore the details with MISA eShop in the article below.

1. Why is it necessary to issue invoices for retail customers who do not request invoices?

From June 1, 2025, according to Decree 70/2025/ND-CP (amending Decree 123/2020/ND-CP), all transactions for the sale of goods and provision of services must issue electronic invoices, regardless of whether the buyer is an organization, individual, or retail customer.

Even when the buyer does not request or does not collect the invoice, the seller is still obligated to issue an invoice and record complete information as required to transmit data to the tax authority.

In simpler terms, even if the buyer is a retail customer and does not request an invoice, the seller must still prepare an electronic invoice and transmit data to the tax authority as required.

This regulation was introduced to move toward a more transparent, synchronized, and accurate tax management system, bringing many practical benefits:

- Increases transparency in sales operations, helping businesses and business establishments easily reconcile revenue and declare taxes accurately;

- Prevents tax fraud, reduces the risk of being considered as “omitting revenue” or “not declaring fully”;

- Creates a unified nationwide database, supporting tax authorities in efficient management and automating the verification and reconciliation process.

2. How to record information on invoices when retail customers do not request invoices

Effective from June 1, 2025, according to Decree 70/2025/ND-CP, buyer information on electronic invoices is more strictly regulated. Therefore, when issuing invoices for retail customers who do not request invoices, sellers need to pay special attention to how content is recorded to ensure validity.

According to Clause 7, Article 1 of Decree 70/2025/ND-CP, which amends and supplements Clause 5 of Decree No. 123/2020/ND-CP dated October 19, 2020 on invoices and documents, the regulations are as follows:

2.1. When the buyer is an organization or business

If the buyer is a business establishment with a tax identification number, the invoice must record accurate, complete, and matching information that has been registered for tax purposes, including:

- Name of the purchasing entity;

- Business registration or tax registration address;

- Tax identification number.

In cases where the name or address is too long, certain common nouns may be abbreviated, such as:

“Ward” → “W.”, “District” → “Dist.”, “City” → “City”, “Limited Liability” → “LLC”, “Joint Stock” → “JSC”.

However, the seller must still ensure absolute accuracy, sufficient identifying elements of the business such as house number, ward, district, province, city.

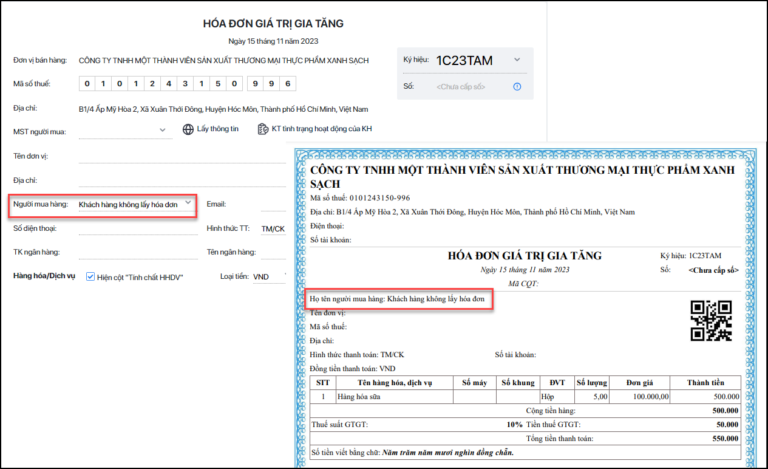

2.2. When issuing invoices for retail customers without tax identification numbers

For individual customers or end consumers (usually retail customers who do not request invoices), the invoice is not required to display the buyer’s tax identification number. In some cases of selling goods and providing specific services to individual consumers as specified in Clause 14 of this Article, the invoice is not required to display the buyer’s name and address.

In cases of selling goods or providing services to foreign customers, buyer information may be replaced with passport number, nationality, or immigration documents, depending on the actual documentation.

2.3. Cases when invoices do not require complete information

If the buyer does not have a tax identification number or personal identification number, the invoice must display the seller’s tax identification number or personal identification number. This regulation ensures that every issued invoice has valid identification information, serving tax management and revenue data reconciliation.

However, according to Clause 14, Article 10 of Decree 123/2020/ND-CP (amended by Decree 70/2025/ND-CP), in some cases where retail customers do not request invoices, sellers may still issue electronic invoices without necessarily having complete buyer information, specifically:

- For electronic invoices for sales at supermarkets and shopping centers where the buyer is a non-business individual, the invoice does not necessarily need to have the buyer’s name, address, tax identification number, or digital signature.

- For electronic invoices for petroleum sales to customers who are non-business individuals, the following indicators are not necessarily required: Name, address, tax identification number of the buyer, digital signature of the buyer.

- For electronic invoices in the form of stamps, tickets, and cards, the invoice does not necessarily need to have the seller’s digital signature (except when stamps, tickets, and cards are electronic invoices coded by tax authorities), buyer indicators (name, address, tax identification number), tax amount, VAT rate. When electronic stamps, tickets, and cards have preset denominations, they do not necessarily need to have indicators for unit of measurement, quantity, unit price.

- For electronic documents of air transport services issued through websites and e-commerce systems following international practices for buyers who are non-business individuals, identified as electronic invoices, the invoice does not necessarily need to have invoice symbol, invoice template symbol, invoice sequence number, VAT rate, buyer’s tax identification number, buyer’s address, seller’s digital signature.

- For electronic invoices for casino operations and gaming activities with prizes, the buyer’s name, address, tax identification number, and digital signature are not necessarily required.

Learn more about how to issue invoices on MISA meInvoice: How to issue VAT invoices for individuals/retail customers/foreigners IN DETAIL

MISA eShop is retail management software with integrated electronic invoicing developed specifically for business establishments and retail stores. On the same platform, users can sell products, manage inventory, track revenue, and issue electronic invoices easily with just a few operations.

In particular, MISA eShop is directly integrated with MISA meInvoice, allowing automatic creation, digital signing, and transmission of electronic invoices to tax authorities immediately after completing transactions. As a result, stores not only comply properly with regulations in Decree 70/2025/ND-CP, but also save time, limit errors, and manage sales data – accounting synchronously and transparently.

Try MISA eShop for free today to experience a comprehensive management – sales – electronic invoicing solution, helping business establishments operate easily and fully comply with new regulations from June 1, 2025.

3. Regulations and penalties for not issuing invoices to retail customers who do not request invoices

Issuing invoices for retail customers who do not request invoices must be implemented in accordance with regulations in Decree 70/2025/ND-CP of the Government, which amends and supplements several articles of Decree 123/2020/ND-CP dated October 19, 2020 on invoices and documents, and Circular 32/2025/TT-BTC of the Ministry of Finance providing implementation guidelines. Accordingly, sellers are responsible for preparing electronic invoices for all transactions of selling goods and providing services, including cases where buyers are individuals who do not request invoices, and must correctly determine the timing of invoice preparation, record all mandatory indicators (name, address, tax identification number or identification number if any), and transmit electronic invoice data to tax authorities within the prescribed time limit.

Proper compliance with regulations helps ensure invoices are valid, lawful, and accepted for tax declaration and settlement, while avoiding the risk of administrative penalties in the field of invoices and documents.

According to Article 24 of Decree 125/2020/ND-CP, penalties for violations of invoice preparation regulations when selling goods and services are as follows:

Article 24. Penalties for violations of invoice preparation regulations when selling goods and services

…

2. Fine from 500,000 VND to 1,500,000 VND for one of the following acts:

a) Not preparing summary invoices in accordance with legal regulations on invoices for selling goods and providing services.

b) Not preparing invoices for goods and services used for promotion, advertising, samples; goods and services used for gifts, donations, exchanges, payment in lieu of wages to employees, except goods for internal circulation, internal consumption to continue the production process.

…

5. Fine from 10,000,000 VND to 20,000,000 VND for not preparing invoices when selling goods and providing services to buyers as required, except for the act specified in Point b, Clause 2 of this Article.

6. Remedial measures: Forced to prepare invoices as required for acts specified in Point d, Clause 4, Clause 5 of this Article when buyers request.

Note: The above fine levels apply to organizations. For taxpayers who are households and business establishments, the fine levels for individuals apply.

Read more: Latest administrative penalties on taxes and invoices for business establishments

4. How to issue electronic invoices for retail customers who do not request invoices according to the latest 2025 regulations

Step 1: Identify the transaction occurrence & timing of invoice preparation

- Every transaction for selling goods or providing services (gifts, promotions, returns…) must prepare an electronic invoice, even if retail customers do not request invoices.

- Determine the timing of invoice preparation: Depending on the type of transaction (immediate sales, periodic service provision, delivery under contract…), invoices must be prepared immediately upon completion of service or upon delivery; in some specific cases, the timing of invoice preparation may be postponed until the end of the tax declaration period.

Step 2: Prepare data & invoice content

- Enter mandatory information: Product name, unit of measurement, quantity, unit price, total amount, VAT rate or non-taxable.

- Seller information: Name, address, tax identification number (TIN), seller’s digital signature.

- Buyer information:

+ If the buyer is a business with a Tax Identification Number: Must record name, address, tax identification number correctly according to tax registration.

+ If the buyer is an individual who does not provide information (retail customer who does not request invoice): Can record “Retail Customer” or “Buyer not requesting invoice”, and leave tax identification number and address blank if exempt under Clause 14, Article 10.

Note: It is best to include a note stating “customer not requesting invoice” to avoid questions when tax authorities inspect.

Step 3: Digital signing & issuing electronic invoices

- After entering complete data, the seller digitally signs the invoice.

- Electronic invoices will be issued as standard format files (XML or PDF with standard data format accepted by tax authorities).

- Electronic invoices must be transmitted to the tax system via protocols and formats specified by the General Department of Taxation.

- Even if customers do not collect, you must still ensure invoice data is sent to tax authorities to record transactions.

Step 5: Store & provide invoices when needed

- Electronic invoices need to be stored for at least the prescribed period (usually 10 years) for inspection and reconciliation purposes.

- If retail customers later request invoices, you can send invoices as PDFs, lookup codes, or send links for customers to view/download themselves.

Step 6: Handle errors if any

- If issued invoices have errors (name, address, unit price, tax rate, goods…), sellers need to make notifications or prepare adjustment/replacement invoices according to new regulations.

- If the same information is incorrect in multiple invoices within the same month, a single adjustment/replacement invoice can be used with an attached list of incorrect invoices according to the prescribed format.

5. Support for issuing electronic invoices to retail customers quickly and in compliance with MISA eShop

Issuing electronic invoices for retail customers seems simple but requires accountants and store owners to master the process of invoice preparation, digital signing, and data transmission to tax authorities in compliance with regulations in Decree 70/2025/ND-CP. To minimize errors and save operation time, many business establishments have chosen MISA eShop – retail management software with integrated electronic invoicing and digital signatures certified by the General Department of Taxation.

When selling at the counter or online, the MISA eShop system will automatically prepare and digitally sign electronic invoices, pre-fill buyer information according to standard templates, then send directly to tax authorities in just a few seconds. All invoice data is synchronized with accounting software and digital signatures, helping stores manage revenue, tax reporting, and store documents transparently with absolute security.

With MISA eShop, business establishments and retail stores can issue invoices quickly, automatically sign digitally, in compliance with regulations, ready for digital transformation roadmap and elimination of lump-sum tax in 2026. Discover MISA eShop now to experience a comprehensive electronic invoicing solution for business establishments and retail stores.